DeFi: Redefining the Future of Loans

Introduction:

Imagine a world where money isn't controlled by big banks but by technology that anyone can access.

where borrowing and lending money are streamlined, eliminating the need for banks, stacks of paperwork, or long approval times. That's what decentralized finance (DeFi) is all about—making financial transactions simple, fast, and fair for everyone, no matter who they are or where they live.

Think of DeFi as a dynamic digital ecosystem where you can borrow, lend, and invest without jumping through hoops or dealing with intimidating bank procedures. Instead of waiting days for approval, everything happens in minutes, thanks to a breakthrough in technology called blockchain.

It functions as a highly secure digital ledger that records every transaction.

Keeps track of ownership, detailing who owns what.

Once recorded, information cannot be changed or tampered with.

Extremely reliable and nearly impossible to cheat.

But DeFi isn't just a cool idea—it's a game-changer for people who've been shut out of traditional banking systems. Whether you're in a remote village or a bustling city, DeFi gives you the power to control your money without relying on anyone else's approval.

It's like taking control of your financial destiny and opening doors to opportunities you never thought possible.

Theory and Background:

Traditional Finance vs. Decentralized Finance:

Let's take a step back and talk a bit about traditional banking. When you've needed to borrow money from a bank, what's been your experience? There's typically a lot of red tape involved—you fill out forms, undergo credit checks, and then wait for the bank's approval.

Why all these formalities and checks? Banks act as intermediaries to ensure responsible loan management and mitigate the risk of default. These procedures are essential to protect the funds they lend and to accurately assess your creditworthiness.

Now, think about it from the bank's perspective: if they didn't have these checks and balances in place, they'd face higher risks of losing money. That's why they often ask for credit and collateral—like a house or car—as a safety net. It's a way for them to secure their investment in case things don't go as planned.

Have you ever found these processes frustrating, or do you appreciate these lengthy procedures?

Let's explore how decentralized finance (DeFi) is reshaping these dynamics.

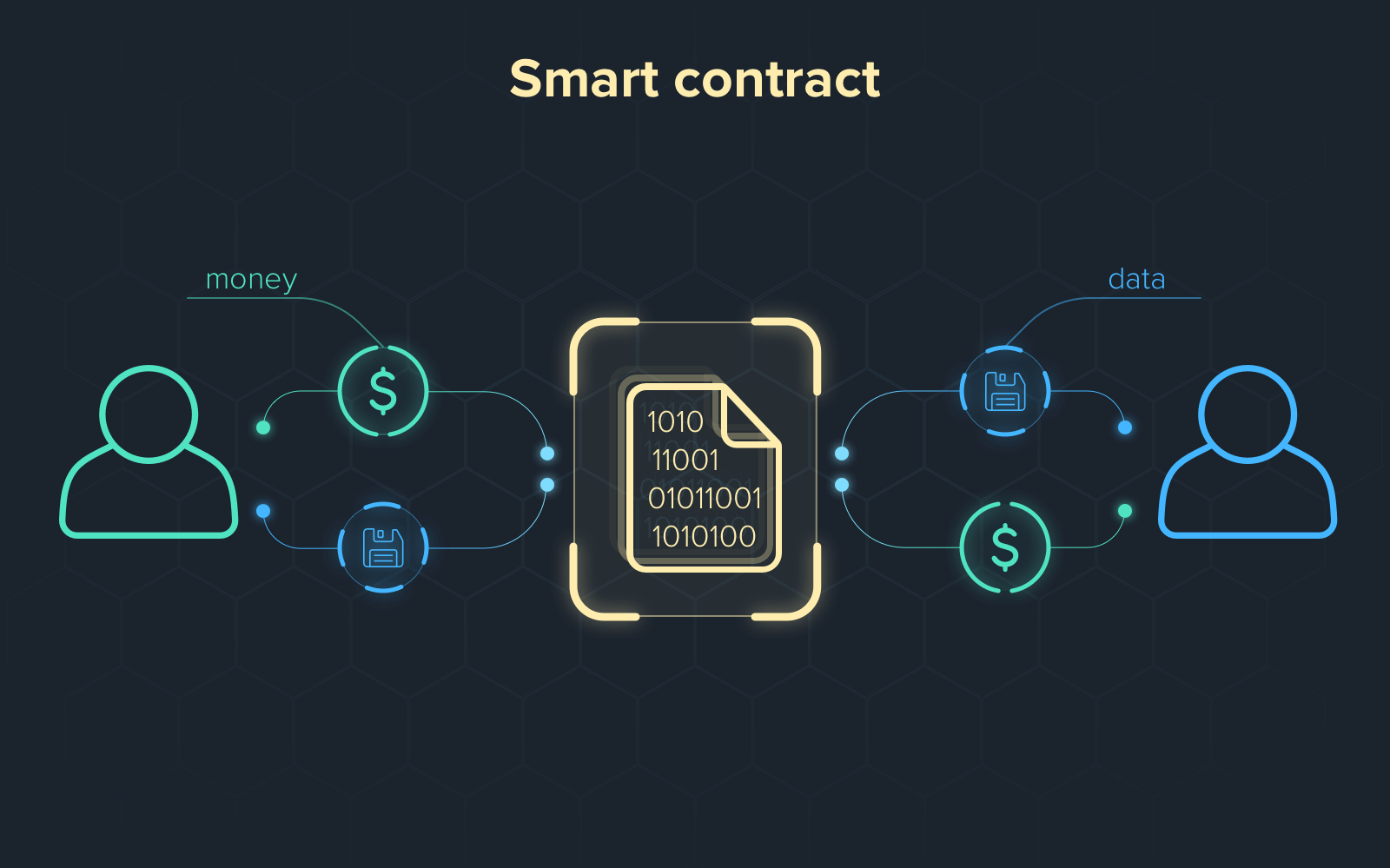

DeFi flips this system on its head by eliminating many of the traditional hurdles associated with borrowing money. Instead of relying on centralized banks, DeFi uses smart contracts—self-executing code on the blockchain that enforces the terms of the loan. These smart contracts automate the process, making it faster, cheaper, and more accessible. With DeFi, there's no need for a bank to oversee transactions, as everything is transparent and tamper-proof on the blockchain.

Let's examine how the time frames differ:

Traditional bank loan processes are notoriously sluggish, with approvals dragging on for days or even weeks. A personal loan may require 1-7 business days, while a mortgage could extend to an agonizing 30-60 day wait.

But in the DeFi universe, time bends to the will of technology. Smart contracts, the backbone of DeFi, streamline lending processes, executing agreements with lightning speed. Picture this: a borrower deposits collateral, and within minutes, a smart contract orchestrates the loan, cutting through red tape and delivering funds in a fraction of the time.

Overcollateralization in DeFi:

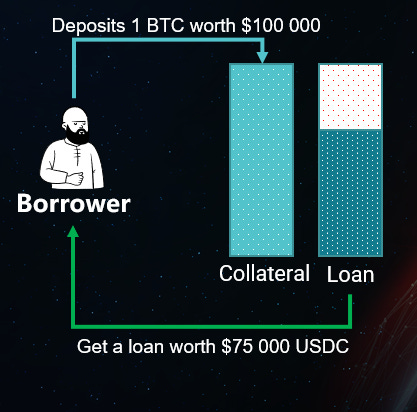

A key feature of DeFi lending is overcollateralization. To borrow $70, you might need to provide $100 worth of cryptocurrency as collateral. This higher collateral requirement acts as a safety net, protecting lenders from the volatility of cryptocurrencies and reducing the risk of default. If a borrower can't repay the loan, the lender can sell the collateral to cover their loss.

But the ingenuity doesn't end there. DeFi platforms employ liquidation mechanisms to safeguard lenders further. If collateral values dip perilously close to the loan amount, that is if the value of the collateral drops and the debt value reaches 82.50% of the collateral value, the position is automatically liquidated, ensuring lenders are protected from market downturns.

For example:

Let's paint a scenario: You provide an asset worth $100 as collateral and borrow $70 against it using a smart contract. Suddenly, the market takes a dip, and your asset is now valued at $60. You've borrowed more than the current value of your collateral—$70 against $60.

Now, if you were in this situation, what would you do? Repay the loan immediately, or would you find yourself in a bit of a bind, like many others might?

Here's where the magic—or rather, the smartness—of the liquidation mechanism comes into play. The smart contract keeps a close watch on your collateral's value. Let's say the protocol has set the liquidation threshold ratio to 82.5%. This means if your borrowed amount becomes 82.5% of your collateral value, liquidation is triggered. In this case, when your $100 collateral drops to $84.85, your $70 loan would become 82.5% of your collateral value ($70 / $84.85 ≈ 0.825 or 82.5%).

At this point, the contract automatically sells your collateral to recover the loan amount plus any liquidation penalties. The remaining funds, after covering the debt and fees, will be returned to your account. For example, if there's a 5% liquidation penalty, $73.50 would be deducted ($70 loan + $3.50 penalty), and you'd receive any leftover amount from your collateral.

It's a bit scary, right? But it's also incredibly smart. This mechanism helps maintain the system's stability by ensuring that loans are backed by sufficient collateral, even in turbulent market conditions. So, what do you think about this approach?

Democratizing Access to Loans:

Here's where DeFi flips the script on traditional finance. In the world of DeFi, your borrowing potential isn't dictated by a credit score; it's governed by the collateral you provide.

Meet Alice and Bob:

Alice has a poor credit score due to financial troubles in the past. Despite having a steady job and reliable income now, she finds it challenging to get a loan from traditional banks. They see her low credit score as a high risk. As a result, Alice is excluded from accessing financial services.

Bob has a good credit score and can easily obtain loans from traditional banks. He doesn't need to worry about getting approval because his financial history is viewed favorably.

In the world of DeFi, the situation changes dramatically:

Alice owns some cryptocurrency, let's say 1.5 ETH (Ethereum), worth $3,000. She needs a $1,000 loan to cover urgent expenses. On a DeFi lending platform, Alice can use her 1.5 ETH as collateral. Since DeFi platforms require overcollateralization, Alice's 1.5 ETH, worth $3,000, is sufficient to secure a $1,000 loan. The smart contract on the platform ensures that her loan is automatically approved as long as she provides the necessary collateral. Her credit score is irrelevant; the collateral she provides is all that matters.

Now, you might wonder, why wouldn't she sell her collateral and get $3,000 instead of just $1,000?

Alright: Imagine you own a piece of land valued at $100,000, but you're hit with a financial crisis and need a $50,000 loan urgently. What would you do in this situation?

You could sell the land to get the cash you need immediately. It seems like a straightforward solution, right? But hold on—what if selling means losing out on potential future gains as the land's value could rise over time?

Consider this: By using the land as collateral for a loan instead, you could secure the funds you need while keeping ownership of an asset that might appreciate in value. It's like keeping your options open for future opportunities while addressing your immediate financial needs.

When faced with such decisions, it's essential to weigh short-term needs against long-term benefits and consider the smartest move for your financial stability and growth.

What do you think you would do in this case? Would you sell the land for quick cash, or would you opt to use it as collateral for a loan?

Bob - with his good credit score, also owns some cryptocurrency. He follows the same process as Alice and secures a loan using his crypto assets as collateral. His good credit score might be beneficial in traditional banking, but in DeFi, it doesn't give him any special advantage over Alice. Both are treated equally based on the collateral they can provide.

DeFi Lending Platforms:

DeFi lending platforms are like online marketplaces for loans, where lenders and borrowers converge in a digital ecosystem powered by innovation. Here's how it unfolds:

Lenders lend their crypto assets, earning interest as funds are loaned. Currently, the returns are quite attractive, with rates up to 15% on your dollar.

Borrowers pledge collateral, unlocking access to instant loans tailored to their needs.

Smart contracts orchestrate transactions seamlessly, automating every facet of the lending process with precision and efficiency.

These platforms herald a new era of financial empowerment, offering speed, accessibility, and transparency unparalleled in traditional finance.

Conclusion:

Get ready for a major shift because the DeFi revolution is here to transform the global financial landscape. With smart contracts on the blockchain replacing human error and bias with automated, fair agreements, our generation has the unique chance to create a more inclusive and fair financial system, breaking down barriers that have existed for centuries. As we move forward, let's embrace the endless possibilities ahead, aiming for a world where financial empowerment knows no boundaries.

While you may have questions about how all of this works, I understand—our journey together is just beginning. In future articles, we'll explore the mechanics, innovations, and transformative impacts of DeFi in greater depth. So, stay tuned and subscribe.